What is single entry and incomplete record?

.

Herein, how do single entry records differ from incomplete records?

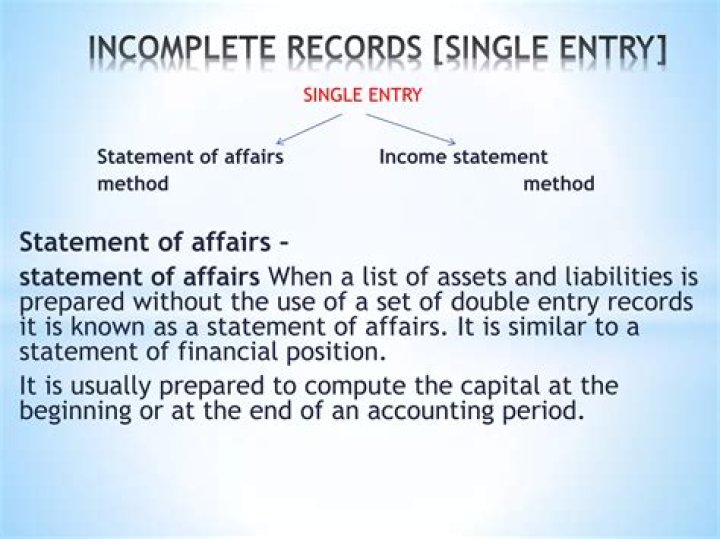

Under the single entry system, a firm maintains only cash account and the accounts of the debtors and the creditors properly. It does not maintain the accounts of expenses, incomes, assets, and liabilities properly. Hence, as the information provided by these records is incomplete, they are known as Incomplete Records.

Additionally, what are the limitations of single entry? The single entry system does not maintain real accounts except cash book. Therefore, it can not reveal the true financial position of the business. The single entry system of book-keeping is incomplete, inaccurate and unscientific. It does not help to check the arithmetical accuracy of the books of accounts.

Similarly, it is asked, what are the features of incomplete records?

Features of Incomplete Records:

- (i) Unsystematic Method:

- (ii) Mixed System for Recording Business Transactions:

- (iii) Lack of Uniformity:

- (iv) Personal Transactions are Mixed up with Business Transactions:

- (v) Based on Estimates:

- (vi) Highly Flexible:

- (vii) Suitable for very Small Business Entities:

Why do incomplete records occur?

Incomplete accounting records occur most often when employees forget to record transactions. When one person is responsible for accounting for all of the transactions, it's less likely for records to get misplaced or to believe that another employee already has made the accounting entry.

Related Question AnswersWhat is the meaning of incomplete records?

Incomplete records refers to a situation in which an organization is not using double-entry bookkeeping. Instead, it is using a more informal accounting system, such as a single-entry system, to maintain a reduced amount of information about its financial results.Is it possible to prepare trial balance in incomplete records?

Broadly speaking, unless a systematic approach to maintenance of records is followed, reliable financial statements cannot be prepared. The limitations of incomplete records are as follows : (a) As double entry system is not followed, a trial balance cannot be prepared and accuracy of accounts cannot be ensured.Who uses single entry system?

Consider the single-entry method if you: Make less than $5 million in annual gross sales or have less than $1 million in gross receipts for inventory sales, according to the IRS. Are a small business that operates as a sole proprietorship, partnership, S Corp, or LLC. Collect customer payments at the point of sale.What is contra entry?

Contra entry is a transaction which involves both cash and bank. Both debit aspect and credit aspect of a transaction get reflected in the cash book. For example: Cash received from debtors and deposited into bank. Cash withdrawn from bank for office use.What do u mean by single entry system?

A single-entry bookkeeping system or single-entry accounting system is a method of bookkeeping relying on a one sided accounting entry to maintain financial information. It's also known as incomplete or unscientific method for recording transactions.Is it possible to use single entry with an accrual system?

Cash-basis accounting uses single-entry bookkeeping. You only record one entry for each business transaction. This is easier to do than accrual, which requires two entries for each transaction. If your business grows big enough, you may need to make a change in accounting method: cash to accrual.What is debit and credit?

A debit is an accounting entry that either increases an asset or expense account, or decreases a liability or equity account. It is positioned to the left in an accounting entry. A credit is an accounting entry that either increases a liability or equity account, or decreases an asset or expense account.How do you prepare financial statements from incomplete records?

Four basic techniques used for incomplete records 1. Construction of opening & closing balance sheets or capital 2. Construction of a cash and / or bank summary 3.Preparation of financial statements using incomplete records

- Introduction of extra capital.

- Withdrawal of capital.

- Profit earned by the business.