What is non owner change in equity?

What is non owner change in equity?

Non-Owner Changes in Equity They are foreign currency transactions, minimum pension liability, adjustments in marketable securities that are held for sale, and the change in value of futures contracts in hedged position.

Where are changes in owners equity reported?

The statement of owner’s equity reports the changes in company equity. The changes that are generally reflected in the equity statement include the earned profits, dividends, inflow of equity, withdrawal of equity, net loss, and so on.

What can change balance of owner’s equity?

The opening balance of the owner’s capital account. Increases to equity from profits or additional capital contributions. Decreases to equity from losses or capital distributions. The closing balance of the owner’s capital account.

What is the formula for change in equity?

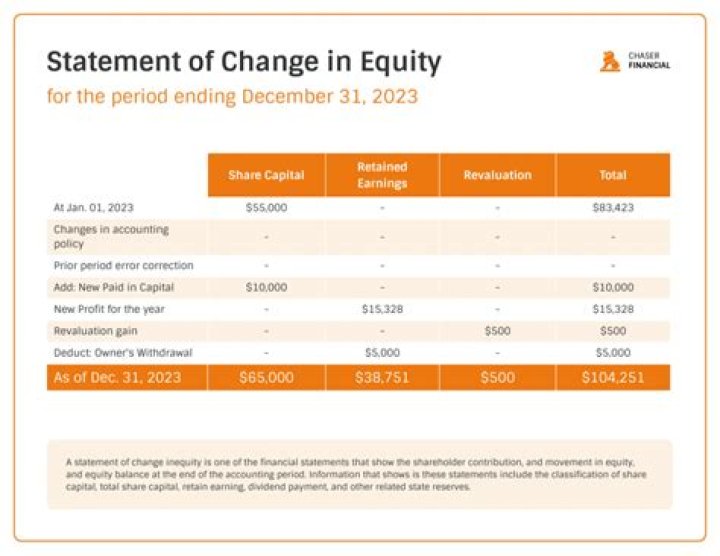

The formula of Statement of Changes in Equity is: Opening Equity balance + Net profit during the period – Dividends (+/-) Other Changes = Closing balance of Equity. Shareholders equity movement over an accounting period are as follows: Net profit or loss after tax during the income year attributable to shareholders.

What is included in OCI?

In business accounting, other comprehensive income (OCI) includes revenues, expenses, gains, and losses that have yet to be realized and are excluded from net income on an income statement. OCI represents the balance between net income and comprehensive income.

How is changes in owner’s equity being prepared?

The Statement of Changes in Owner’s Equity is prepared second to the Income Statement. Again, the most appropriate source of information in preparing financial statements would be the adjusted trial balance. Nonetheless, any report with a complete list of updated accounts may be used.

What is Statement of Changes in Equity in accounting?

A statement of change in equity (also referred to as statement of retained earnings) is a business’ financial statement that measures the changes in owners’ equity throughout a specific accounting period. It covers the following elements: Net profit or loss. Accumulated reserves and retained earnings.

What is owner’s equity?

Stockholders’ equity, also referred to as shareholders’ or owners’ equity, is the remaining amount of assets available to shareholders after all liabilities have been paid. Stockholders’ equity might include common stock, paid-in capital, retained earnings, and treasury stock.

What affects owner’s equity?

The main accounts that influence owner’s equity include revenues, gains, expenses, and losses. Owner’s equity will increase if you have revenues and gains. Owner’s equity decreases if you have expenses and losses. If your liabilities become greater than your assets, you will have a negative owner’s equity.

Why there are changes in equity?

Why is the Statement of Changes in Equity Needed? The difference between the assets and liabilities from one accounting period to the next will give you the movement in equity. This information can be obtained from the balance sheet of the entity.

What is equity formula?

Equity is the value left in a business after taking into account all liabilities. Total equity is the value left in the company after subtracting total liabilities from total assets. The formula to calculate total equity is Equity = Assets – Liabilities.