What is a tax-free F reorganization?

What is a tax-free F reorganization?

An “F” reorganization is a type of tax-free reorganization under Internal Revenue Code Section 368(a)(1)(F), which includes a mere change in identity or form of one corporation. F reorganizations are typically used to effectuate a tax-free shift of a single operating company.

Are reorganizations taxable?

Reorganizations, while not generally taxable at the entity level, are not completely tax-free to the selling shareholders. A reorganization is immediately taxable to the target’s shareholders to the extent they receive non-qualifying consideration, or “boot”.

What is a tax-free transaction?

This type of transaction is deemed to be “tax-free” because the parent company is still able to divest the business it wants to separate from, but the company does not incur capital gains tax on the divestiture, which would be the case in an outright sale of the business unit to another company.

Do you need a new EIN for F reorg?

The previously assigned EIN should be used by the surviving corporation in a statutory merger and in a reincorporation qualifying as an F reorganization. A new EIN should be requested by the new corporation in a consolidation and in any reincorporation transaction not qualifying as an F reorganization.

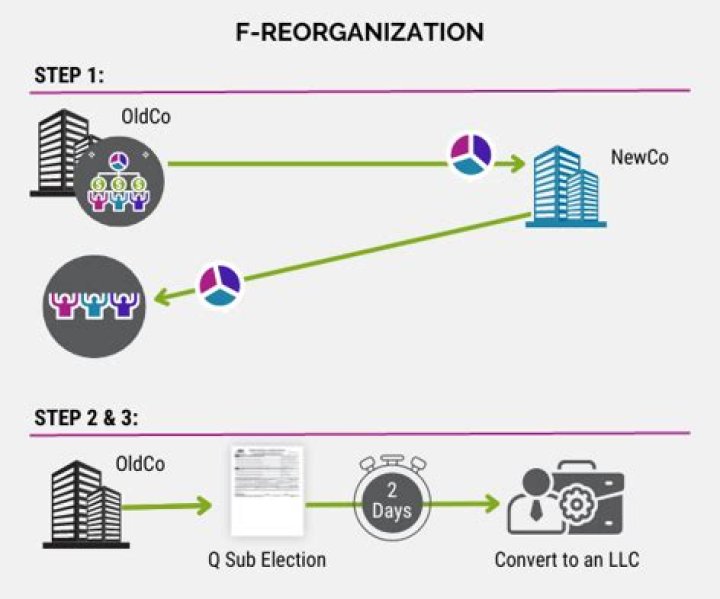

Can an LLC do an F reorganization?

The F Reorganization can facilitate a freeze when you have an existing corporation by creating a two-tier structure where a corporation owns the preferred shares or units of a subsidiary corporation or LLC, and then new common shares or units are issued to new owners/investors in the subsidiary.

Can a C Corp do an F reorg?

While F reorganizations can also be used with C corporations, an F reorganization is particularly well suited for a variety of transactions involving S corporations. All section references herein, other than to Regulations, are to the Internal Revenue Code of 1986, as amended. Reg. § 1.368-2(m)(1).

How does an F reorg work?

Are mergers tax free?

The federal tax code provides for tax free mergers and acquisitions in certain situations. In tax-free mergers, the acquiring company uses its stock as a significant portion of the consideration paid to the acquired company.

What is the reason for tax exemption?

Through tax-exemptions, governments support the work of nonprofits and receive a direct benefit. Nonprofits benefit society. Nonprofits encourage civic involvement, provide information on public policy issues, encourage economic development, and do a host of other things that enrich society and make it more vibrant.

What is the continuity of interest requirement that applies to reorganizations?

What is the Continuity of Interest Doctrine? The Continuity of Interest Doctrine was intended to ensure that a stockholder in an acquired company, who continued to hold an interest in the successor corporation or continuing entity created after the reorganization, would not be taxed.

Does a QSub file a tax return?

There is no separate federal income tax return for a QSub. Its operations are reported in the S corporation’s federal income tax return, thus providing a de facto consolidated return for the S corporation and its QSub.