What does implied volatility tell us?

.

People also ask, what does implied volatility tell you?

Implied volatility represents the expected volatility of a stock over the life of the option. Conversely, as the market's expectations decrease, or demand for an option diminishes, implied volatility will decrease. Options containing lower levels of implied volatility will result in cheaper option prices.

Beside above, is Implied volatility good or bad? So when implied volatility increases after a trade has been placed, it's good for the option owner and bad for the option seller. Conversely, if implied volatility decreases after your trade is placed, the price of options usually decreases. That's good if you're an option seller and bad if you're an option owner.

Also know, what is a good implied volatility?

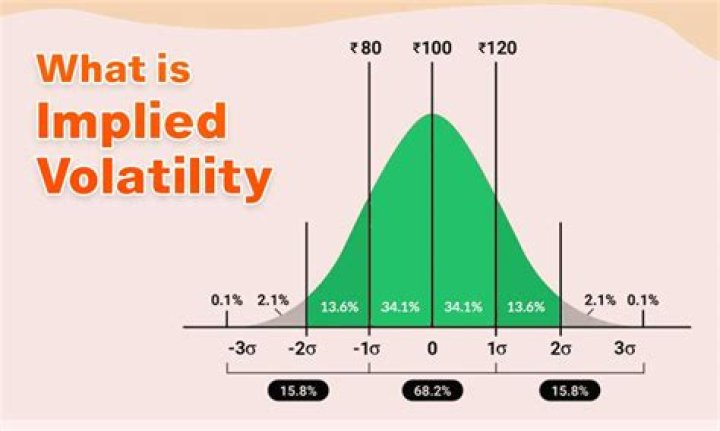

Implied volatility (commonly referred to as volatility or IV) is one of the most important metrics to understand and be aware of when trading options. In the example of a $200 stock with an IV of 25%, it would mean that there is an implied 68% probability that the stock is between $150 and $250 in one year.

How is implied volatility used in trading?

You use the same formula but you don't calculate option value. Instead you take the market price of the option as its intrinsic value and then work backward and calculate the volatility. This is the volatility that is implied in the option price and is called the implied volatility.

Related Question AnswersHow do you trade volatility?

Volatility Trading There are several approaches to trade implied and realized market volatility. One is to use exchange-traded instruments, such as VIX futures contracts and related exchange-traded notes (ETNs). In this approach traders buy or sell VIX index futures, depending on their volatility expectations.How do you interpret volatility?

In most cases, the higher the volatility, the riskier the security. Volatility is often measured as either the standard deviation or variance between returns from that same security or market index. In the securities markets, volatility is often associated with big swings in either direction.Why is volatility important?

Market Performance and Volatility Investors can use this data on long term stock market volatility to align their portfolios with the associated expected returns. The effects of volatility and risk are consistent across the spectrum.How do you trade low volatility?

Here are three options strategies you can use during these low volatility times:- 1) Put/Call Debit Spreads. Make some directional bets on overbought or oversold stocks.

- 2) Ratio Spreads. If your directional assumption is extremely strong, you can use a ratio spread.

- 3) Put/Call Calendars.

What is volatility skew?

Volatility Skew refers to the difference in implied volatility of each opposite, equidistant option. The current volatility skew in the market results in puts trading richer than calls, because the IV in OTM puts is higher than the equivalent OTM calls.How do I get long volatility?

For the average investor there are five ways to go long on VIX:- Buy a leveraged exchange-traded product (ETP) that tends to track the daily percentage moves of the VIX index.

- Buy Barclays' VXX (short term), VXZ (medium-term) Exchange Traded Note (ETN) or one of their competitors that have jumped into this market.

What does VIX stand for?

The CBOE Volatility Index (VIX) is a measure of expected price fluctuations in the S&P 500 Index options over the next 30 days. The VIX, often termed as the "fear index," is calculated in real time by the Chicago Board Options Exchange (CBOE).What is considered low implied volatility?

Implied volatility shows the market's opinion of the stock's potential moves, but it doesn't forecast direction. If the implied volatility is high, the market thinks the stock has potential for large price swings in either direction, just as low IV implies the stock will not move as much by option expiration.What does IV crush mean?

Volatility crush is a term used in options trading to describe the swift reduction in implied volatility of an option after the underlying stock's earnings are announced or some other major news event.How do you trade options when volatility is high?

Six Options Strategies for High-Volatility Trading Environments- High-vol bullish strategies include short puts and short put vertical spreads.

- High-vol bearish strategies include short call vertical spreads and “unbalanced” butterfly spreads.

- High-vol neutral strategies include iron condors and long butterfly spreads.

How do you predict implied volatility?

First, divide the number of days until the stock price forecast by 365, and then find the square root of that number. Then, multiply the square root with the implied volatility percentage and the current stock price. The result is the change in price.How does volatility affect option prices?

Unlike interest rates, volatility significantly affects the option prices. The higher the volatility of the underlying asset, the higher is the price for both call options and put options. This happens because higher volatility increases both the up potential and down potential.What is the difference between volatility and implied volatility?

In contrast to historical volatility, which looks at actual asset prices in the past, implied volatility (IV) looks ahead. Implied volatility can be derived from the price of an option. Specifically, implied volatility is the expected future volatility of the stock that is implied by the price of the stock's options.What is option volatility?

Volatility, in relation to the options market, refers to fluctuation in the market price of the underlying asset. Higher implied volatility indicates that greater option price movement is expected in the future. Another form of volatility that affect options is historic volatility, also known as statistical volatility.What is RVOL?

Relative Volume or RVOL is an indicator used to help determine the amount of volume change over a given period of time. It is often used to help traders determine how in-play a ticker is. General rule of thumb is the higher the RVOL, the more in play a stock is.Is volatility a good measure of risk?

Volatility gives certain information about the dispersion of returns around the mean, but gives equal weight to positive and negative deviations. Moreover, it completely leaves out extreme risk probabilities. Volatility is thus a very incomplete measure of risk.Is volatility a standard deviation?

Standard deviation is a statistical term that measures the amount of variability or dispersion around an average. Standard deviation is also a measure of volatility. Generally speaking, dispersion is the difference between the actual value and the average value.Which stocks are most volatile?

Most volatile stocks- 5 Years.

- 10 Years. Advanced Micro Devices Inc. AMD, +1.43% 19.50. 17.32. 17.64. 870% 470% 759% Celgene Corp. US:CELG. 9.42.

- 3 years.

- 5 years.

- 10 years.

- 3 Years.

- 5 Years.

- 10 Years. Nektar Therapeutics. NKTR, +1.23% Biotechnology. 29.80. 24.84. 20.15. 214% 222% 904% Freeport-McMoRan Inc. FCX, -2.93% Precious Metals.