What are the two basic categories of adjusting entries?

The two basic categories of adjusting entries are prepaids and accruals. Two examples of prepaids are prepaid expenses (such as Prepaid Rent and Office Supplies) and unearned revenues (such as Unearned Service Revenue).

.

Moreover, what are the two basic categories of adjusting entries provide two examples of each?

Provide two examples of each. The two basic categories of adjusting entries are prepaids and accruals. Office Supplies) and unearned revenues (such as Unearned Service Revenue). Expense) and accrued revenues (such as Accrued Service Revenue).

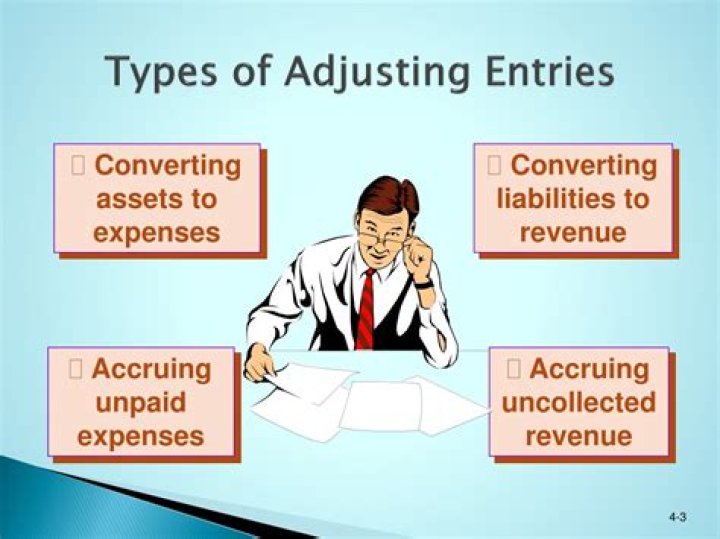

Beside above, what are the 5 types of adjusting entries? The five types of adjusting entries

- Accrued revenues. When you generate revenue in one accounting period, but don't recognize it until a later period, you need to make an accrued revenue adjustment.

- Accrued expenses.

- Deferred expenses.

- Deferred expenses.

- Depreciation expenses.

Then, what are the basic types of adjusting entries?

Types of Adjusting Entries

- Accrued revenues. Under the accrual method of accounting, a business is to report all of the revenues (and related receivables) that it has earned during an accounting period.

- Accrued expenses.

- Deferred revenues.

- Deferred expenses.

- Depreciation expense.

What are two examples of adjustments?

Examples of such accounting adjustments are:

- Altering the amount in a reserve account, such as the allowance for doubtful accounts or the inventory obsolescence reserve.

- Recognizing revenue that has not yet been billed.

- Deferring the recognition of revenue that has been billed but has not yet been earned.

What are general journal entries?

A general journal entry includes the date of the transaction, the titles of the accounts debited and credited, the amount of each debit and credit, and an explanation of the transaction also known as a Narration.What are adjusting journal entries?

An adjusting journal entry involves an income statement account (revenue or expense) along with a balance sheet account (asset or liability). Estimates are adjusting entries that record non-cash items, such as depreciation expense, allowance for doubtful accounts, or the inventory obsolescence reserve.What is meant by adjusting entry?

Adjusting entries are journal entries made at the end of an accounting cycle to update certain revenue and expense accounts and to make sure you comply with the matching principle. The matching principle states that expenses have to be matched to the accounting period in which the revenue paying for them is earned.Why are adjusting entries important?

Adjusting entries are necessary because a single transaction may affect revenues or expenses in more than one accounting period and also because all transactions have not necessarily been documented during the period.What is adjustment?

Adjustment, in psychology, the behavioral process by which humans and other animals maintain an equilibrium among their various needs or between their needs and the obstacles of their environments. A sequence of adjustment begins when a need is felt and ends when it is satisfied.What entries should be reversed?

The only types of adjusting entries that may be reversed are those that are prepared for the following:- accrued income,

- accrued expense,

- unearned revenue using the income method, and.

- prepaid expense using the expense method.

What is accrual entry?

An accrual is a journal entry that is used to recognize revenues and expenses that have been earned or consumed, respectively, and for which the related cash amounts have not yet been received or paid out.What are the four main classifications of journal entries?

There are four types of adjusting journal entries used in a small business.- Adjusting for Accrued Revenues. Accrued revenue occurs when you make a sale and collect payment at a later date.

- Adjusting for Accrued Expenses.

- Adjusting for Deferred Revenues.

- Adjusting for Deferred Expenses.