How much can you contribute to a 529 plan in Virginia?

How much can you contribute to a 529 plan in Virginia?

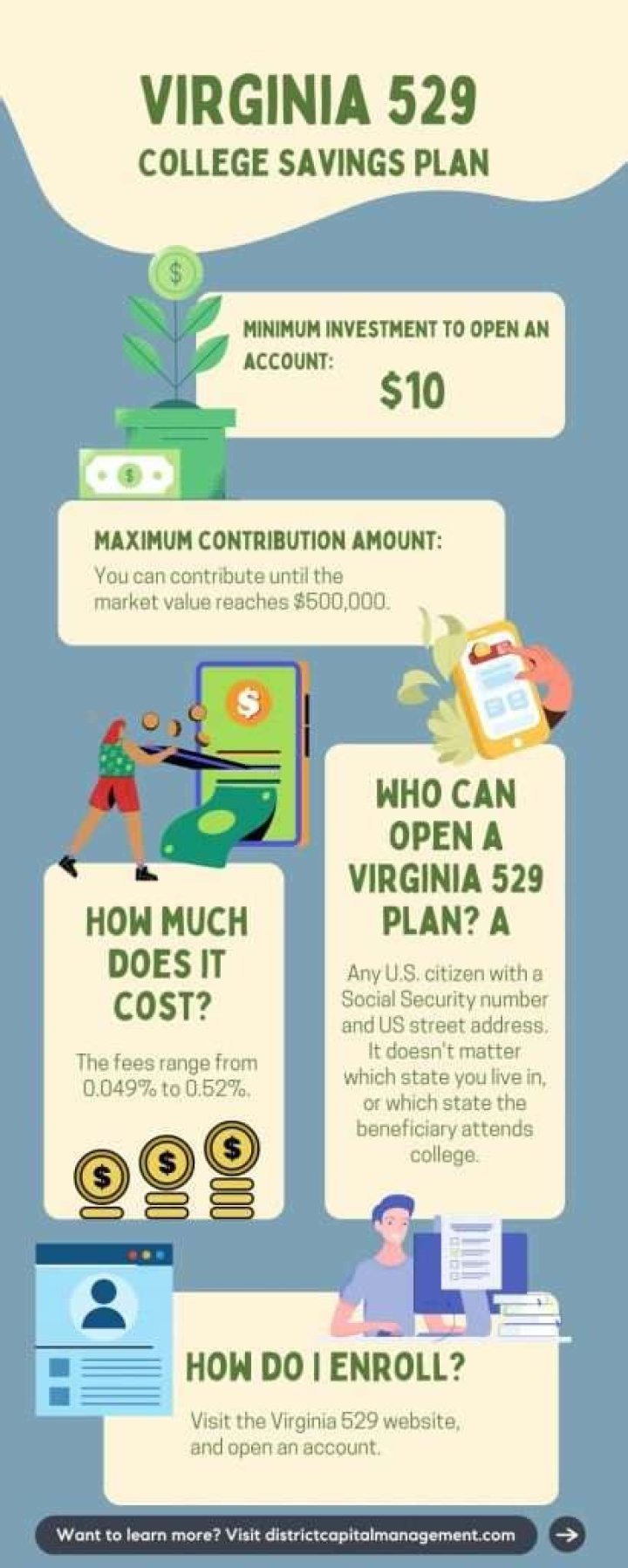

Contributions to a Virginia 529 plan of up to $4,000 per account per year are deductible in computing Virginia taxable income, with an unlimited carryforward of excess contributions. Contributions are fully deductible in the year of contribution for taxpayers at least 70 years of age.

What is the max 529 contribution for 2020?

Because the funding includes graduate tuition and related costs, 529 plan maximum contributions range from $300,000-$500,000 for each beneficiary. For example, California’s maximum contribution amount is $475,000 per beneficiary. Michigan’s maximum contribution for a 529 Savings Plan is $500,000.

How much can you put in a 529 each year?

States with the highest aggregate limits

| State | Aggregate limit |

|---|---|

| Missouri | $550,000 |

| New Hampshire | $542,000 |

| California | $529,000 |

| New York, Rhode Island | $520,000 |

What can Virginia529 funds be used for?

Virginia529 accounts can fund many qualified higher education expenses for eligible four-year colleges, two-year colleges, graduate schools, trade schools, training programs and tuition at private or religious K-12 schools.

Does contributing to 529 reduce taxable income?

1. 529 plans offer unsurpassed income tax breaks. Although contributions are not deductible, earnings in a 529 plan grow federal tax-free and will not be taxed when the money is taken out to pay for college. This has been a huge incentive for Americans to save for college.

Is it better for a parent or grandparent to own a 529 plan?

How Grandparent 529 Plans Affect Financial Aid. Overall, 529 plans have a minimal effect on financial aid. But, the FAFSA treats parent-owned accounts more favorably. For example, you report 529 plans assets as parent assets, which can only reduce aid eligibility by a maximum 5.64% of the account value.

Why is a 529 plan a bad idea?

It could hurt your child’s chances of getting financial aid Any distributions from a 529 plan that’s owned by a third-party are counted as untaxed income, and they may hurt your child’s chances of qualifying for financial aid, including grants, work-study programs, and subsidized loans.

Is VA 529 worth it?

For most people, getting a Virginia 529 plan is a good idea. It charges low fees and gives you access to exclusive FDIC-insured investment options. It also allows you to use third-party advisors for more savvy investment options. Plus, it’s the only way for Virginia residents to be eligible for state tax deductions.

Can a Virginia529 plan be used for off-campus housing?

The short answer is: Yes, room and board expenses for off-campus housing – including a parent’s home – may be reimbursed through a 529 plan, but not necessarily the full cost.

Are 529 contributions tax deductible?

Unlike an IRA, contributions to a 529 plan are not deductible and therefore do not have to be reported on federal income tax returns. What’s more, the investment earnings in your account are not reportable until the year they are withdrawn. 529 plans save taxpayers billions of dollars on their income taxes.

Is there age limit for 529 plans?

Any U.S. citizen or resident alien 18 years old or older can open a 529 account. Usually, the beneficiary is a child, grandchild or younger relative. However, an adult can also open a 529 plan to save for his or her own higher education costs since there are no age limits.

What is a 529 plan?

529 plans are tax-advantaged accounts that can be used to cover educational expenses from kindergarten through graduate school.