How do you calculate non-controlling interest in IFRS?

How do you calculate non-controlling interest in IFRS?

To calculate the NCI of the income statement, take the subsidiaries net income and multiply by the NCI percentage. For example, if the organization owns 70% of the subsidiary and a minority partner owns 30% and subsidiaries net income say $1M. The non-controlling interest would be calculated as $1M x 30% = $300k.

How are non-controlling interests measured?

Non-controlling interests are measured at the net asset value of entities and do not account for potential voting rights. Most shareholders of public companies today would be classified as holding a non-controlling interest, with even a 5% to 10% equity stake considered to be a large holding in a single company.

How is NCI measured?

So what is non-controlling interest (NCI)? To calculate goodwill, the NCI at the date of acquisition is introduced as a consolidation adjustment. as a proportion of net assets, meaning it is measured based on the net assets at acquisition and is said to give rise to proportional goodwill.

What is a non-controlling interest under IFRS?

International Accounting Standard 27 (IAS 27) defines non-controlling interest as “the equity in a subsidiary not attributable, directly or indirectly, to a parent”. This means that any position that holds less than 50% of the outstanding voting rights is deemed to be a non-controlling interest.

How is holding minority interest calculated?

The book value, or the net asset value of a company, is its total assets less the intangible assets (patents, goodwill) and liabilities. You then proceed to multiply the book value by the percentage of the subsidiary owned by the minority shareholders.

Where is non-controlling interest on income statement?

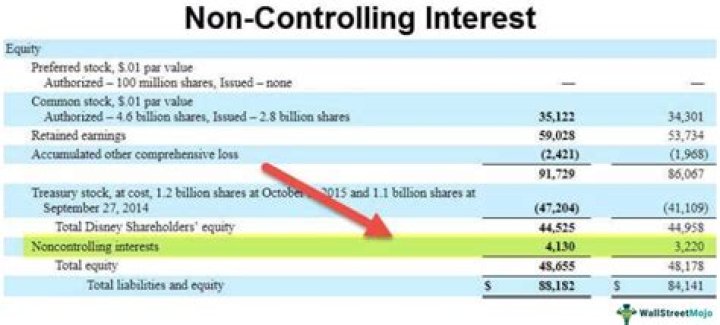

Accounting treatment Under the International Financial Reporting Standards, the non-controlling interest is reported in accordance with IFRS 5 and is shown at the very bottom of the Equity section on the consolidated balance sheet and subsequently on the statement of changes in equity.

Why is NCI measured at fair value?

Conceptually the use of the measurement of NCI at Fair Value is considered superior. This is because it is consistent in that all the other ingredients in the calculation of goodwill also at fair value. This is again consistent with the way that we consolidate the other assets of the subsidiary.

How is NCI proportionate method calculated?

It can be calculated as the sum of proportionate share in net assets i.e. $8.75 million (=25% of $35 million) plus proportionate share in net fair value differential i.e. $1.25 million (=25% of $5 million).

How is CFS minority interest calculated?

The main steps included are:

- Note down the total value of the subsidiary company same as it is shown on the balance sheet of the company.

- Multiply the subsidiary value by the percentage owned by other parties.

- Note down the value of minority interest under the section “shareholder’s equity” in the balance sheet.

How do you calculate minority interest IFRS?

The calculation of minority interest is relatively simple and requires the use of minority shareholders’ percentage ownership of a subsidiary. This measurement is then reported on the parent’s consolidated balance sheet and income statement in accordance with IFRS or U.S. GAAP rules.