How do I account for a bearer plant?

How do I account for a bearer plant?

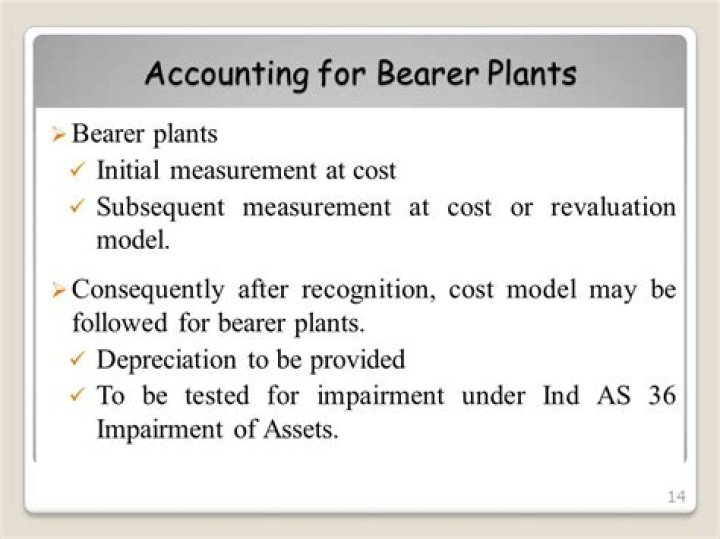

A bearer plant should be accounted for as property, plant and equipment (PPE) in accordance with Ind AS 16. Therefore, companies will now be required to measure bearer plants initially at cost and will thereafter have an option to apply either the cost or the revaluation model.

What is the difference between bearer plant and biological asset?

Biological assets are measured at fair value to correctly reflect the future economic benefits that will be received from the biological transformation. Mature bearer plants are, however, fully grown and biological transformation is no longer significant in generating future economic benefits.

What is bearer plant as per IAS 16?

A bearer plant is defined as “a living plant that: is used in the production or supply of agricultural produce; is expected to bear produce for more than one period; and. has a remote likelihood of being sold as agricultural produce, except for incidental scrap sales.”

Is Grapevine a bearer plant?

The following are not bearer plants: Plants cultivated for sale only (e.g. in a garden centre) Annual crops (e.g. wheat) Produce growing on a bearer plant (e.g. grape on a vine)

Which accounting standard does not apply to produce on bearer plant?

Thus, AS 10 applies to Bearer plants but is not applicable to the produce on bearer plants. Wasting assets that include mineral rights, expenditure on the exploration for an extraction of minerals, oil, natural gas and similar other non-regenerative resources.

Is Bearer plant a biological asset?

Bearer biological assets are self-regenerating assets other than consumable biological assets, for example dairy cattle rather than beef cattle, grape vines and fruit trees.

What are the 41 accounting standards?

The objective of IAS 41 is to establish standards of accounting for agricultural activity – the management of the biological transformation of biological assets (living plants and animals) into agricultural produce (harvested product of the entity’s biological assets).

Can dismantling costs be capitalized?

Its purchase price of fixed assets. Entity might incur costs to bringing the asset to the location and condition and these costs should also be capitalized.

What is bearer plant as per AS 10?

Bearer plant here means a plant that is: used in the production or supply of agricultural produce. Is anticipated to give produce for more than 12 months. Has a remote chance of being sold as an agricultural produce except for incidental scrap sales.

Is Apple a biological asset?

Biological Assets are assets that are living – for example, trees, animals, or cannabis. Biological assets also include crops grown by farmers – e.g., corn, tomatoes – as well as grapevines, cannabis, trees, and any produce coming from trees, such as apples.

What is agriculture in accounting?

IAS 41 Agriculture sets out the accounting for agricultural activity – the transformation of biological assets (living plants and animals) into agricultural produce (harvested product of the entity’s biological assets). The standard generally requires biological assets to be measured at fair value less costs to sell.

What does IAS mean in accounting?

International Accounting Standards

International Accounting Standards (IAS) are older accounting standards issued by the International Accounting Standards Board (IASB), an independent international standard-setting body based in London. The IAS were replaced in 2001 by International Financial Reporting Standards (IFRS).

How should a bearer plant be accounted for?

A bearer plant should be accounted for as property, plant and equipment (PPE) in accordance with Ind AS 16. Therefore, companies will now be required to measure bearer plants initially at cost and will thereafter have an option to apply either the cost or the revaluation model.

What is the IASB’s new proposal for bearer plants?

The IASB proposes to include bearer plants within the scope of IAS 16. Consequently, entities would be permitted to choose either the cost model or the revaluation model for mature bearer plants subject to the requirements in IAS 16. All other biological assets related to agricultural activity will remain under the fair value model in IAS 41.

What is the accounting literature on bearer plants in India?

With respect to bearer plants, before the introduction of the Companies (Indian Accounting Standards) Rules, 2015, there was no specific accounting literature in India that dealt with agriculture.

How are bearer plants classified under IAS 12?

Bearer plants related to agricultural activity are classified as property, plant and equipment under IAS 12 in the current financial period. (Effective date: For annual periods beginning on or after 1 January 2016).